Loan Prepayment vs Foreclosure – What’s the Difference? (2026 Guide)

Many borrowers aim to repay their loans early to reduce interest costs and become debt-free faster. When it comes to closing a loan early, two commonly used terms appear: loan prepayment and loan foreclosure.

Although both involve repaying a loan before its scheduled tenure, they are not exactly the same.

Understanding the difference between these two options helps borrowers make better financial decisions and avoid unnecessary charges.

In this guide, we will explain how loan prepayment and foreclosure work, their benefits, potential charges, and when each option is suitable.

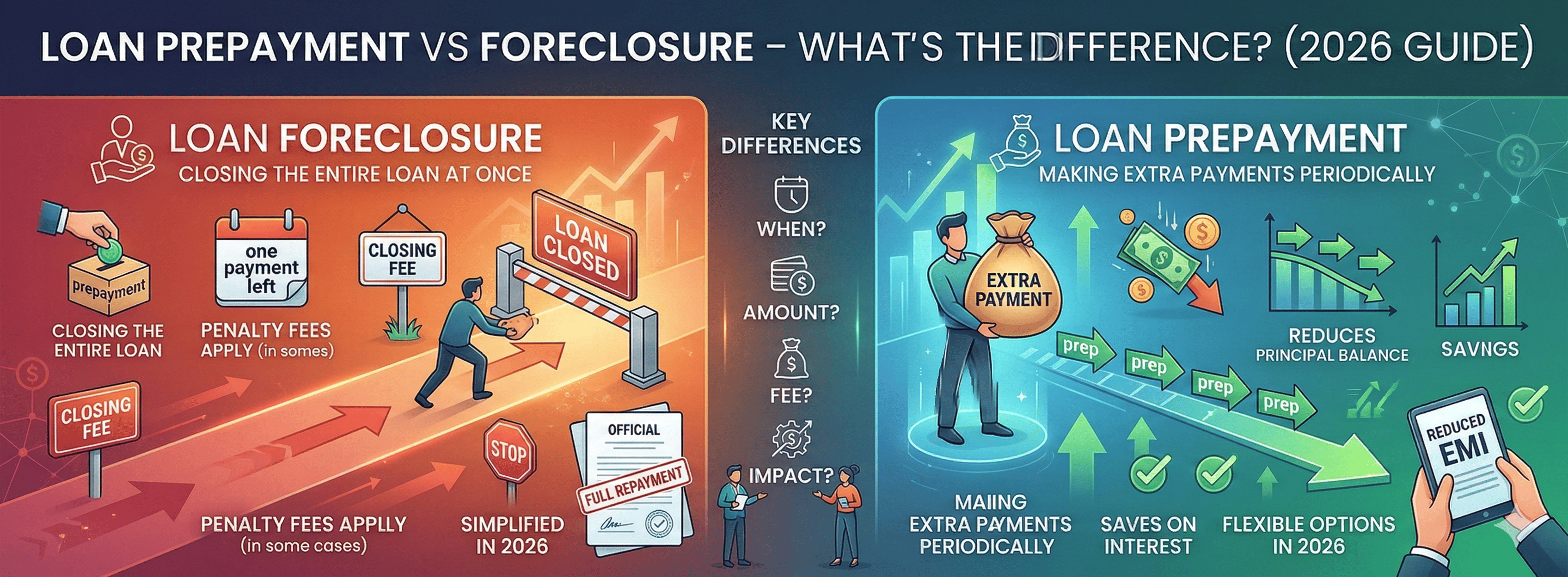

What is Loan Prepayment?

Loan prepayment refers to paying a portion of the outstanding loan amount before the scheduled due date.

Instead of paying only the monthly EMI, borrowers choose to pay an additional amount toward the principal loan balance.

This reduces the outstanding loan amount and may either:

• Reduce future EMIs, or

• Reduce the total loan tenure

Prepayment helps borrowers save on interest costs over the long term.

Example of Loan Prepayment

Consider the following example.

Loan amount: ₹10,00,000

Interest rate: 10%

Loan tenure: 10 years

After a few years, the borrower makes a partial prepayment of ₹2,00,000.

As a result:

• The outstanding principal decreases

• Future interest charges reduce

• The loan tenure or EMI may decrease

This helps borrowers repay the loan faster and save interest.

What is Loan Foreclosure?

Loan foreclosure refers to repaying the entire remaining loan balance before the end of the loan tenure.

Once foreclosure is completed, the loan account is closed permanently and the borrower has no further EMI obligations.

This is often done when borrowers receive a large amount of money from sources such as:

• Bonuses

• Investments

• Property sales

• Inheritance

By foreclosing the loan, borrowers avoid paying future interest.

Example of Loan Foreclosure

Let us consider another example.

Loan amount: ₹5,00,000

Remaining balance after 3 years: ₹2,20,000

If the borrower decides to pay ₹2,20,000 in one payment, the loan is fully closed.

No further EMIs are required after foreclosure.

Key Differences Between Prepayment and Foreclosure

Feature — Loan Prepayment — Loan Foreclosure

Meaning — Partial repayment of loan — Full repayment of loan

Loan Status — Loan continues — Loan closes completely

EMI Payments — Continue after prepayment — EMIs stop after foreclosure

Interest Savings — Partial savings — Maximum interest savings

Frequency — Can be done multiple times — Done once to close loan

Both options help borrowers reduce interest costs but work differently.

Charges for Loan Prepayment and Foreclosure

Some lenders charge prepayment or foreclosure fees depending on the loan type.

Typical charges may include:

Prepayment charges: 1% – 3% of prepaid amount

Foreclosure charges: 2% – 5% of outstanding loan amount

However, in India, many lenders do not charge foreclosure fees on floating-rate home loans.

Borrowers should always check loan terms before making early repayments.

Benefits of Loan Prepayment

Reduces Interest Cost

Paying extra toward the principal reduces future interest charges.

Flexible Repayment

Borrowers can make partial payments whenever they have extra funds.

Shorter Loan Tenure

Prepayment can significantly reduce the loan duration.

Benefits of Loan Foreclosure

Become Debt-Free Faster

Foreclosing a loan removes all future EMI obligations.

Save Maximum Interest

Since the loan is closed completely, borrowers avoid future interest payments.

Financial Freedom

Loan foreclosure improves financial flexibility.

When Should You Choose Loan Prepayment?

Prepayment may be a better option if:

• You receive occasional extra income

• You want to reduce loan tenure gradually

• You do not want to close the loan completely

It is useful for borrowers who want to reduce interest costs while maintaining financial liquidity.

When Should You Choose Loan Foreclosure?

Foreclosure may be suitable if:

• You have enough funds to close the entire loan

• Interest rates are high

• You want to eliminate debt completely

However, borrowers should ensure they maintain sufficient savings before foreclosing a loan.

Factors to Consider Before Prepayment or Foreclosure

Before repaying a loan early, borrowers should consider the following.

Check Foreclosure Charges

Some lenders charge penalties for early loan closure.

Maintain Emergency Savings

Avoid using all savings to close a loan.

Compare Interest vs Investment Returns

Sometimes it may be better to invest extra money instead of repaying low-interest loans.

Review Loan Terms

Always read the loan agreement carefully to understand prepayment rules.

Frequently Asked Questions

What is the difference between prepayment and foreclosure?

Prepayment involves paying part of the loan early, while foreclosure means closing the entire loan before the tenure ends.

Does prepayment reduce EMI?

Yes, prepayment may reduce EMI or shorten the loan tenure depending on the lender's policy.

Are foreclosure charges mandatory?

Not always. Many lenders do not charge foreclosure fees on floating-rate home loans.

Can I prepay my personal loan?

Yes, most personal loans allow partial prepayment after a certain lock-in period.

Conclusion

Loan prepayment and foreclosure are both effective strategies for reducing debt and saving interest costs.

Prepayment allows borrowers to reduce their loan balance gradually, while foreclosure helps close the loan entirely and eliminate future EMIs.

Before choosing either option, borrowers should carefully review loan terms, check for applicable charges, and ensure they maintain sufficient financial reserves.

Making informed decisions about loan repayment can significantly improve financial stability and help borrowers achieve long-term financial freedom.