Introduction

Your CIBIL score plays a crucial role in determining whether your loan gets approved or rejected. Most banks and NBFCs in India require a CIBIL score of 750 or above for easy loan approval.

If your score is low, don’t worry. In this guide, we will show you practical and proven ways to improve your CIBIL score fast — even within 30 days.

What is a CIBIL Score?

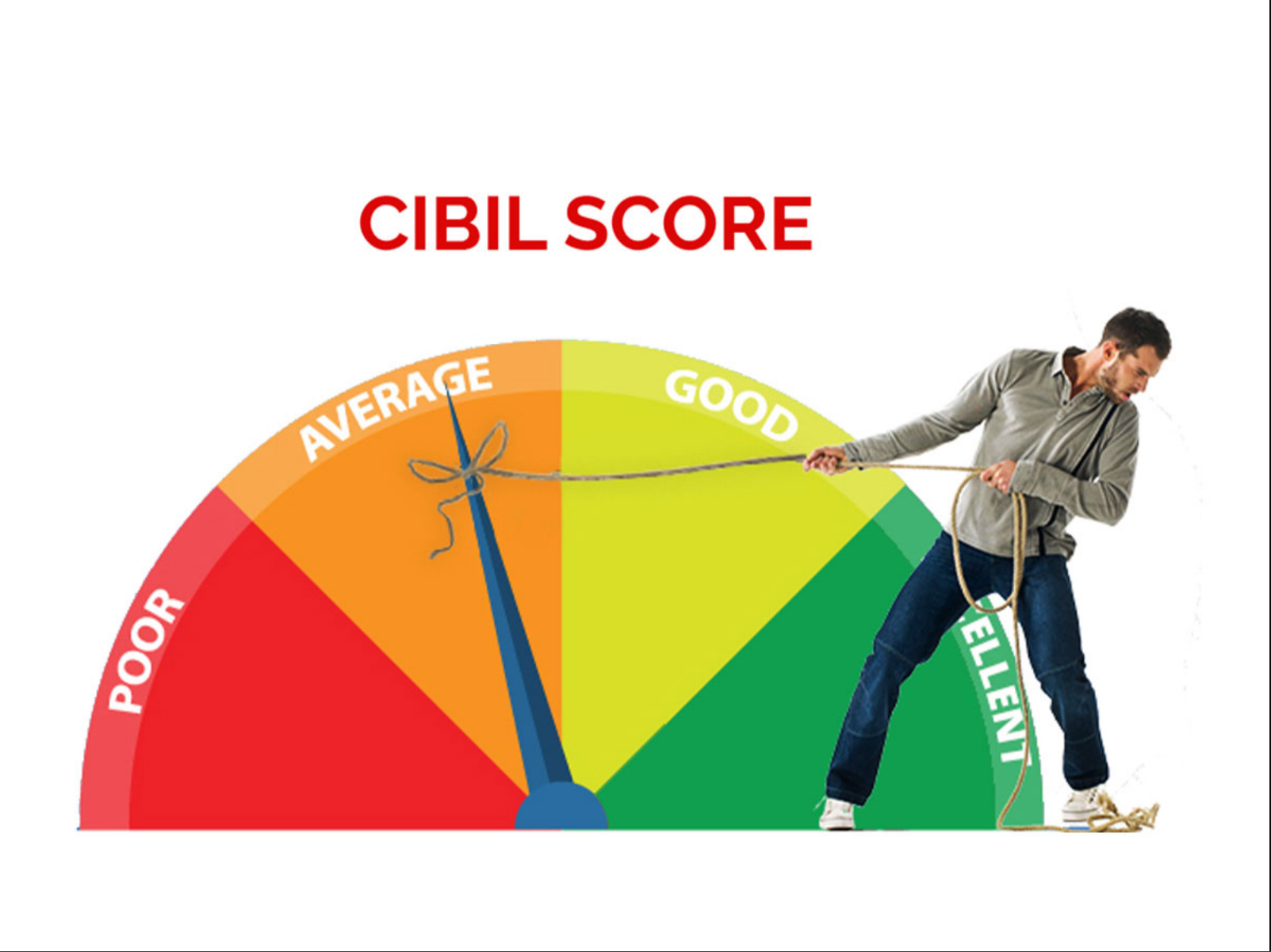

A CIBIL score is a three-digit number ranging from 300 to 900, representing your creditworthiness.

- 750 – 900 → Excellent

- 700 – 749 → Good

- 650 – 699 → Average

- Below 650 → Poor

The higher your score, the better your chances of loan approval at lower interest rates.

Why Is Your CIBIL Score Low?

Before improving your score, understand why it dropped:

- Late EMI payments

- Credit card outstanding dues

- High credit utilization ratio

- Multiple loan applications in short time

- Loan settlement instead of closure

- Errors in CIBIL report

Identifying the issue is the first step toward improvement.

10 Proven Ways to Improve CIBIL Score in 30 Days

1. Pay All EMIs and Credit Card Bills on Time

Payment history accounts for nearly 35% of your credit score. Even one missed EMI can reduce your score significantly.

Set reminders or enable auto-debit to avoid delays.

2. Reduce Credit Card Utilization Below 30%

If your credit card limit is ₹1,00,000, try to keep usage below ₹30,000.

High utilization signals financial stress to lenders.

3. Clear Overdue Amounts Immediately

If you have any pending dues, clear them as soon as possible. Even partial payments can positively impact your score.

4. Avoid Applying for Multiple Loans

Every loan application triggers a hard inquiry. Too many inquiries reduce your credit score.

Apply strategically.

5. Check Your CIBIL Report for Errors

Sometimes incorrect entries affect your score.

- Wrong late payment record

- Closed loan showing active

- Duplicate accounts

You can dispute errors directly on the CIBIL website.

6. Convert Credit Card Dues into EMI

If you cannot clear full dues, convert them into structured EMI payments. This reduces credit utilization ratio.

7. Do Not Close Old Credit Cards

Old credit history improves your credit age, which positively impacts your score.

8. Increase Credit Limit (Without Increasing Usage)

If your bank increases your limit and you keep usage low, your utilization ratio improves.

9. Maintain a Healthy Credit Mix

Having both secured loans (home loan, auto loan) and unsecured loans (personal loan) helps maintain a balanced profile.

10. Avoid Loan Settlements

Loan settlement negatively impacts your credit profile. Always aim for proper loan closure.

How Much Can Your Score Improve in 30 Days?

If you:

- Clear overdue payments

- Reduce credit card usage

- Avoid new loan applications

You may see an improvement of 20 to 80 points within one month, depending on your profile.

Minimum CIBIL Score Required for Loans

- Personal Loan: 700+

- Home Loan: 750+

- Credit Card: 700+

- Business Loan: 650+

Even with low CIBIL, approval is possible with expert assistance.

Can You Get Loan with Low CIBIL Score?

Yes, but:

- Interest rates may be higher

- Loan amount may be lower

- Approval chances reduce

At NSV Finserv, we help clients improve their profiles before applying to increase approval chances.

Frequently Asked Questions (FAQs)

Does checking CIBIL score reduce it?

No. Checking your own score is a soft inquiry and does not affect it.

How long does it take to improve CIBIL score?

Noticeable improvement can be seen within 30–60 days with disciplined actions.

What is considered a good CIBIL score in 2026?

A score above 750 is considered good.

Final Thoughts

Improving your CIBIL score is not complicated — it just requires discipline and the right strategy.

If your loan was rejected due to low CIBIL score, don’t apply again immediately. Fix your profile first.

👉 Need help improving your credit profile or applying for the right loan?

Contact NSV Finserv today for expert guidance and better approval chances.