How Banks Decide Loan Interest Rates in India (2026 Complete Guide)

When applying for any type of loan—whether it is a home loan, personal loan, car loan, or business loan—one of the most important factors borrowers consider is the interest rate.

Loan interest rates determine how much extra money borrowers must pay in addition to the principal loan amount.

However, many people wonder how banks actually decide these interest rates and why different borrowers receive different loan rates.

In this guide, we will explain the major factors that influence loan interest rates in India and how banks determine the cost of borrowing.

What is Loan Interest Rate?

A loan interest rate is the percentage charged by lenders on the borrowed amount.

It represents the cost of borrowing money from a bank or financial institution.

For example, if you borrow ₹5,00,000 at an interest rate of 10%, the lender charges interest on the outstanding loan balance until it is fully repaid.

Interest rates may be fixed or floating, depending on the loan agreement.

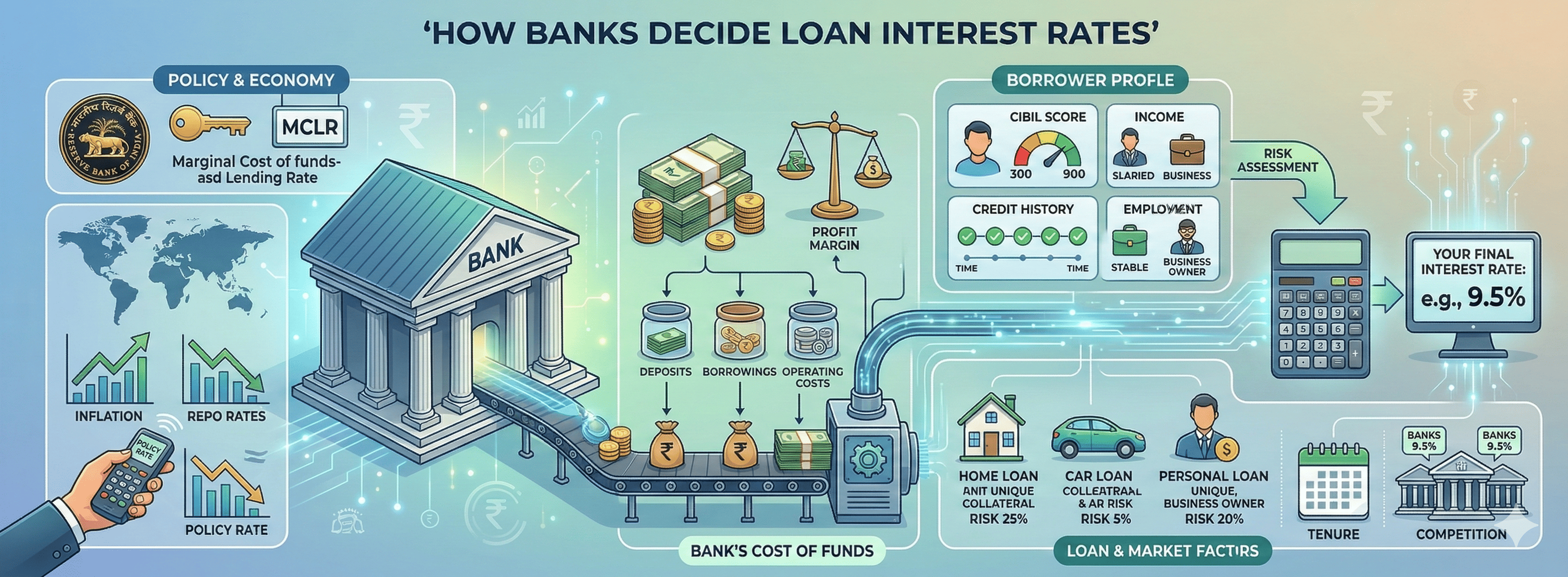

Role of RBI in Loan Interest Rates

The Reserve Bank of India (RBI) plays a major role in influencing interest rates across the banking system.

One of the most important benchmark rates set by RBI is the Repo Rate.

What is Repo Rate?

The repo rate is the interest rate at which RBI lends money to commercial banks.

When the RBI increases the repo rate:

• Borrowing becomes expensive for banks

• Banks may increase loan interest rates

When the repo rate decreases:

• Banks can borrow money more cheaply

• Loan interest rates may decrease

This is why loan rates often change after RBI policy announcements.

Benchmark Lending Rates Used by Banks

Banks use different benchmark systems to determine loan interest rates.

Some common benchmark rates include:

External Benchmark Lending Rate (EBLR)

Many loans are now linked directly to external benchmarks such as the RBI repo rate.

MCLR (Marginal Cost of Lending Rate)

MCLR was previously widely used by banks to determine lending rates based on their cost of funds.

Base Rate

Older loans may still be linked to base rate systems used by banks before MCLR.

These benchmarks help ensure transparency in how interest rates are calculated.

Factors That Influence Loan Interest Rates

Banks consider several factors when deciding the interest rate offered to borrowers.

Credit Score

Your credit score is one of the most important factors.

Credit Score — Impact on Interest Rate

750+ — Lower interest rates

700–749 — Competitive rates

650–699 — Higher rates

Below 650 — Very high rates or rejection

A higher credit score indicates responsible borrowing behavior and lower risk.

Income and Repayment Capacity

Banks assess your income to determine whether you can comfortably repay the loan.

Higher income usually results in:

• Higher loan eligibility

• Lower interest rates

Stable employment and consistent income also improve loan terms.

Type of Loan

Different loan types carry different levels of risk.

Loan Type — Typical Interest Rate

Home Loans — Lower rates (secured loans)

Car Loans — Moderate rates

Personal Loans — Higher rates (unsecured loans)

Credit Cards — Very high interest rates

Secured loans usually have lower interest rates because lenders hold collateral.

Loan Tenure

The length of the loan tenure also affects interest rates.

Longer loan tenures may result in:

• Higher total interest costs

• Slightly higher interest rates

Shorter tenure loans may offer better rates but higher EMIs.

Loan Amount

Large loan amounts sometimes attract lower interest rates because lenders earn more interest overall.

However, lenders also assess risk before approving large loans.

Relationship with the Bank

Existing customers may receive better loan offers.

Factors that help include:

• Long banking relationship

• Salary account with the bank

• Good repayment history

Banks often provide preferential rates to loyal customers.

Economic Conditions

Interest rates are also influenced by broader economic conditions.

Factors include:

• Inflation levels

• RBI monetary policy

• Banking liquidity

• Economic growth

When inflation rises, interest rates often increase to control borrowing.

Fixed vs Floating Interest Rates

Banks typically offer two types of loan interest structures.

Fixed Interest Rate

The interest rate remains constant throughout the loan tenure.

Advantages include predictable EMIs and stable repayment plans.

Floating Interest Rate

Floating rates change based on benchmark interest rates such as the RBI repo rate.

This means EMIs may increase or decrease depending on market conditions.

How Borrowers Can Get Lower Interest Rates

Borrowers can take several steps to improve their chances of getting better loan rates.

Maintain High Credit Score

Pay all EMIs and credit card bills on time.

Reduce Existing Debt

Lower debt levels improve your financial profile.

Compare Multiple Lenders

Different banks offer different loan rates.

Choose Shorter Tenure

Shorter tenures may offer lower interest rates.

Build Relationship with Bank

Maintaining a salary account or long-term relationship may result in better loan offers.

Frequently Asked Questions

Why do different banks offer different loan interest rates?

Each bank has its own lending policies, risk assessment models, and cost of funds.

Does credit score affect interest rate?

Yes, borrowers with higher credit scores typically receive lower interest rates.

Do loan interest rates change over time?

Floating interest rates can change depending on RBI policy and market conditions.

Are secured loans cheaper than unsecured loans?

Yes, secured loans such as home loans generally have lower interest rates.

Conclusion

Loan interest rates in India are influenced by several factors including RBI policies, benchmark lending rates, borrower credit profiles, loan type, and overall economic conditions.

Banks evaluate these factors carefully to determine the cost of lending and the risk associated with each borrower.

Understanding how banks decide loan interest rates can help borrowers improve their financial profile, secure better loan terms, and reduce borrowing costs.

By maintaining a strong credit score, managing debts responsibly, and comparing lenders, borrowers can significantly improve their chances of obtaining loans at competitive interest rates.