Top Government Subsidy Schemes for Home Buyers in India (2026 Guide)

Buying a home is one of the biggest financial decisions most people make in their lifetime. To make housing more affordable, the Government of India has introduced several subsidy schemes for home buyers.

These schemes help reduce the cost of purchasing a house by providing benefits such as interest subsidies, lower loan interest rates, and financial assistance.

Government housing programs are especially beneficial for first-time home buyers, middle-income families, and economically weaker sections of society.

In this guide, we will explore the top government subsidy schemes available for home buyers in India and how you can benefit from them.

Why Government Housing Schemes Are Important

Housing affordability remains a major concern in India, especially in urban areas where property prices are high.

Government subsidy programs aim to:

• Encourage home ownership

• Support low and middle-income families

• Promote affordable housing development

• Reduce the financial burden of home loans

These schemes make it easier for eligible individuals to buy their first home.

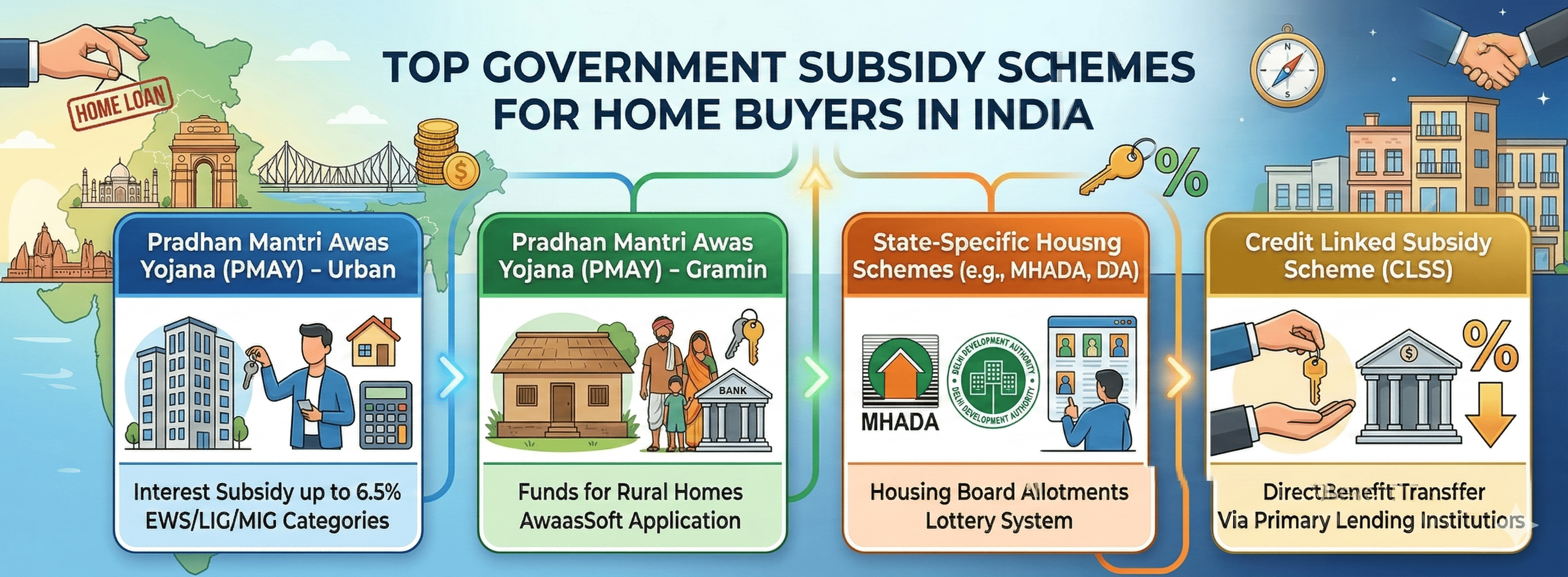

Pradhan Mantri Awas Yojana (PMAY)

One of the most important housing schemes in India is the Pradhan Mantri Awas Yojana (PMAY).

PMAY aims to provide “Housing for All” by offering interest subsidies on home loans to eligible beneficiaries.

Under this scheme, borrowers receive interest subsidies through the Credit Linked Subsidy Scheme (CLSS).

PMAY Income Categories

PMAY divides beneficiaries into different income groups.

Income Category — Annual Household Income

Economically Weaker Section (EWS) — Up to ₹3 Lakhs

Lower Income Group (LIG) — ₹3 Lakhs to ₹6 Lakhs

Middle Income Group I (MIG I) — ₹6 Lakhs to ₹12 Lakhs

Middle Income Group II (MIG II) — ₹12 Lakhs to ₹18 Lakhs

Each category receives different subsidy benefits.

PMAY Interest Subsidy Benefits

PMAY offers interest subsidies depending on the income group.

Income Group — Interest Subsidy

EWS / LIG — 6.5% subsidy

MIG I — 4% subsidy

MIG II — 3% subsidy

The subsidy amount is credited directly to the borrower’s loan account, reducing the principal loan amount and EMI burden.

Eligibility for PMAY Subsidy

To qualify for PMAY benefits, applicants must meet certain conditions.

Common eligibility requirements include:

• Applicant must not own a pucca house anywhere in India

• The property must be purchased for residential use

• Applicant must belong to an eligible income category

• Property must be located in an approved city or town

First-time home buyers benefit the most from this scheme.

State Government Housing Schemes

In addition to central government programs, many state governments offer their own housing subsidy schemes.

These schemes vary by state but generally aim to support affordable housing development.

Examples include:

• Maharashtra Housing Scheme

• Delhi Affordable Housing Program

• Tamil Nadu Housing Board Schemes

• Karnataka Affordable Housing Programs

These programs often provide additional financial support or reduced property prices.

Interest Subsidy Scheme for Housing the Urban Poor (ISHUP)

The Interest Subsidy Scheme for Housing the Urban Poor was introduced to help lower-income urban households obtain affordable housing loans.

The scheme provides interest subsidies to reduce loan repayment costs for economically weaker families.

Although newer programs such as PMAY have become more prominent, similar subsidy mechanisms continue under updated government housing initiatives.

Benefits of Government Housing Subsidy Schemes

Government housing schemes offer several advantages for home buyers.

Reduced Loan Burden

Interest subsidies lower the effective cost of borrowing.

Lower EMIs

Since the subsidy reduces the principal loan amount, monthly EMIs become more affordable.

Encourages Home Ownership

These programs help more families purchase their first home.

Financial Support for Middle-Income Families

Many schemes are designed to support middle-income groups as well.

How to Apply for Home Loan Subsidy

The process of applying for government housing subsidies is relatively straightforward.

Step 1: Apply for a home loan through a bank or housing finance company.

Step 2: Provide income and property details.

Step 3: The lender checks eligibility for government subsidy schemes.

Step 4: If eligible, the subsidy amount is credited directly to the loan account.

Borrowers do not need to apply separately in many cases, as lenders usually process subsidy applications automatically.

Documents Required for Subsidy Schemes

Applicants typically need the following documents.

• Aadhaar Card

• PAN Card

• Income proof

• Property documents

• Bank statements

• Home loan sanction letter

Additional documents may be required depending on the specific scheme.

Tips for First-Time Home Buyers

Before applying for a home loan under government subsidy schemes, consider the following tips.

Check Eligibility Carefully

Ensure you meet income and property ownership criteria.

Compare Lenders

Different banks may offer different interest rates and processing fees.

Understand Loan Terms

Review interest rates, tenure options, and repayment terms.

Maintain Good Credit Score

A strong credit score improves loan approval chances.

Frequently Asked Questions

What is PMAY subsidy?

PMAY subsidy is a government interest subsidy provided on home loans to eligible home buyers.

Who can apply for PMAY?

First-time home buyers belonging to eligible income categories can apply for PMAY.

How much subsidy can I get under PMAY?

Subsidy depends on income category and loan amount, but it can significantly reduce total interest cost.

Can salaried individuals apply for government housing schemes?

Yes, salaried individuals can apply if they meet income eligibility criteria.

Conclusion

Government housing subsidy schemes such as Pradhan Mantri Awas Yojana (PMAY) have made home ownership more accessible for millions of Indians.

These programs provide valuable financial support through interest subsidies and affordable housing initiatives.

If you are planning to purchase your first home, exploring government subsidy schemes can significantly reduce your home loan burden and make home ownership more affordable.

Before applying, always check eligibility requirements, compare lenders, and understand loan terms to make an informed financial decision.