Fixed vs Floating Interest Rate – Which Loan Option Is Better? (2026 Guide)

When applying for a loan, one of the most important decisions borrowers must make is choosing between a fixed interest rate and a floating interest rate.

The type of interest rate you choose directly affects your monthly EMI, total interest cost, and long-term financial planning.

While fixed rates offer stability and predictable payments, floating rates can change based on market conditions and central bank policies.

In this guide, we will explain the difference between fixed and floating interest rates, their advantages and disadvantages, and how to choose the best option for your loan.

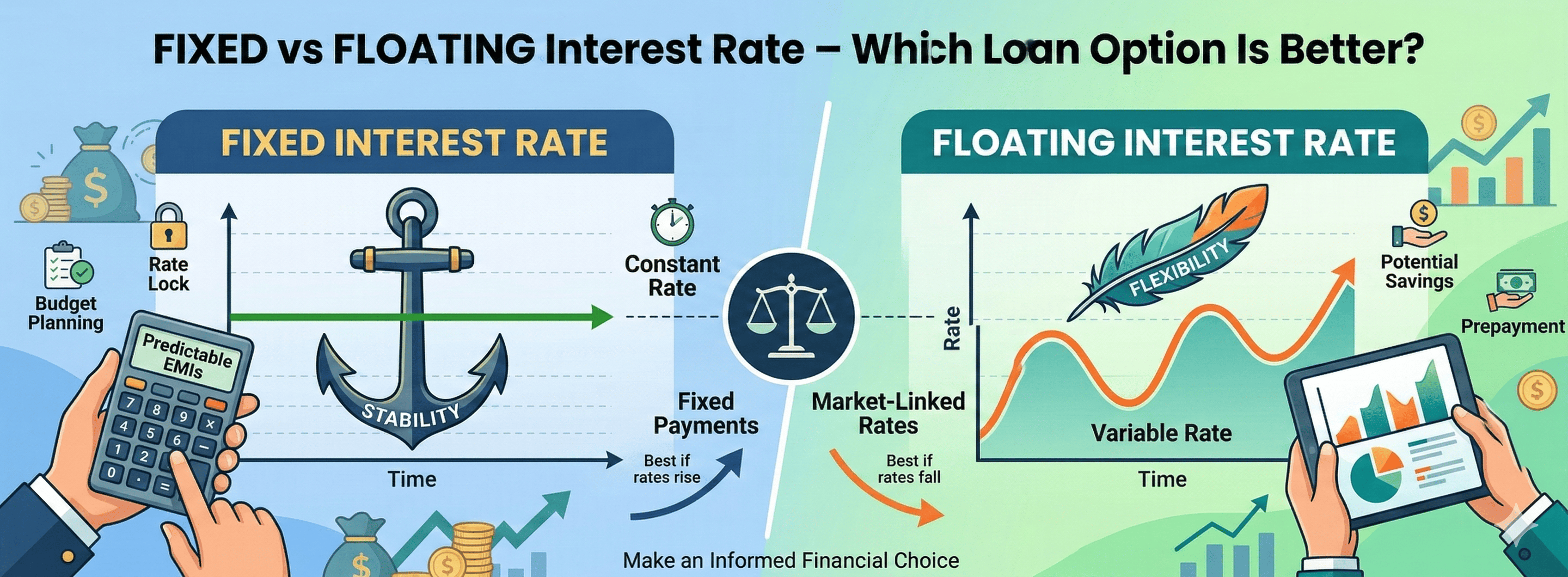

What is a Fixed Interest Rate?

A fixed interest rate means that the interest rate on your loan remains constant throughout the loan tenure or for a predefined period.

This means your monthly EMI remains the same, regardless of changes in market interest rates.

For example, if you take a loan with a fixed interest rate of 9%, your EMI will remain unchanged even if market interest rates increase or decrease.

Advantages of Fixed Interest Rate Loans

Stable Monthly Payments

Your EMI remains constant throughout the loan tenure, making financial planning easier.

Protection from Interest Rate Increases

If market interest rates rise, your loan interest rate remains unchanged.

Better Budget Planning

Since EMI remains fixed, borrowers can plan their finances more accurately.

Disadvantages of Fixed Interest Rate Loans

Higher Interest Rates

Fixed-rate loans often have slightly higher interest rates compared to floating-rate loans.

Limited Benefit if Interest Rates Fall

If market interest rates decrease, borrowers do not benefit from lower rates.

Limited Flexibility

Some lenders may charge prepayment or foreclosure penalties on fixed-rate loans.

What is a Floating Interest Rate?

A floating interest rate (also known as a variable interest rate) changes based on market conditions.

Floating rates are usually linked to benchmark rates such as:

• RBI Repo Rate

• MCLR (Marginal Cost of Lending Rate)

• External Benchmark Lending Rate

When these benchmark rates change, your loan interest rate and EMI may also change.

Advantages of Floating Interest Rate Loans

Lower Initial Interest Rates

Floating-rate loans typically start with lower interest rates compared to fixed-rate loans.

Benefit When Interest Rates Decrease

If market interest rates fall, your loan interest rate may also decrease.

Lower Prepayment Charges

Most floating-rate loans allow partial or full prepayment without penalties.

Disadvantages of Floating Interest Rate Loans

EMI Fluctuations

Monthly EMI may increase if interest rates rise.

Uncertainty in Long-Term Costs

It becomes harder to predict the total loan cost over time.

Market Dependency

Floating rates are influenced by economic conditions and central bank policies.

Fixed vs Floating Interest Rate Comparison

Feature — Fixed Interest Rate — Floating Interest Rate

Interest Rate Stability — Constant — Changes with market conditions

EMI Amount — Fixed — May increase or decrease

Initial Interest Rate — Usually higher — Usually lower

Risk Level — Low risk — Moderate risk

Benefit if Rates Fall — No — Yes

Financial Planning — Easier — Less predictable

Which Loans Offer Fixed and Floating Rates?

Different types of loans offer both interest rate options.

Home Loans

Home loans commonly offer both fixed and floating interest rate options.

Many borrowers choose floating rates because they often start lower.

Personal Loans

Most personal loans come with fixed interest rates, meaning EMI remains constant.

Car Loans

Car loans may offer either fixed or floating interest rates depending on the lender.

When Should You Choose Fixed Interest Rate?

A fixed interest rate may be a good option if:

• You prefer predictable EMIs

• Interest rates are expected to rise

• You want stable financial planning

• Your budget requires fixed monthly payments

When Should You Choose Floating Interest Rate?

A floating interest rate may be better if:

• Market interest rates are expected to decrease

• You want lower initial interest rates

• You plan to prepay the loan early

• You can handle small EMI fluctuations

Example of Fixed vs Floating Loan

Consider a loan of ₹30 Lakhs for 20 years.

Fixed Rate Example:

Interest Rate: 9%

EMI: Stable for entire tenure

Floating Rate Example:

Interest Rate: Starts at 8.5%

EMI may increase or decrease based on RBI policy changes.

Over time, floating-rate loans may become cheaper if interest rates decline.

Tips for Choosing the Right Loan Interest Type

Check Market Interest Trends

If interest rates are rising, fixed rates may be safer.

Compare Multiple Lenders

Different banks offer different interest rate structures.

Understand Loan Terms

Check prepayment charges and rate reset policies.

Consider Financial Stability

Choose the option that fits your income stability and risk tolerance.

Frequently Asked Questions

Which is better – fixed or floating interest rate?

Both options have advantages. Fixed rates offer stability, while floating rates may offer lower interest costs.

Do floating interest rates change frequently?

Floating rates usually change when benchmark interest rates are revised.

Are personal loans fixed or floating?

Most personal loans come with fixed interest rates.

Can I switch from fixed to floating interest rate?

Some lenders allow borrowers to convert their loan type, usually with a conversion fee.

Conclusion

Choosing between fixed and floating interest rates is an important financial decision when taking a loan.

Fixed rates offer stability and predictable EMIs, making them ideal for borrowers who prefer financial certainty. Floating rates, on the other hand, may offer lower interest costs but come with some risk due to market fluctuations.

Before selecting a loan type, borrowers should evaluate interest rate trends, financial stability, and long-term repayment plans.

Making the right choice can help reduce total interest costs and ensure comfortable loan repayment over time.