What is Debt-to-Income Ratio (DTI) and Why It Matters for Loans (2026 Guide)

When you apply for a loan, banks evaluate several financial factors before approving your application. One of the most important metrics lenders consider is the Debt-to-Income Ratio (DTI).

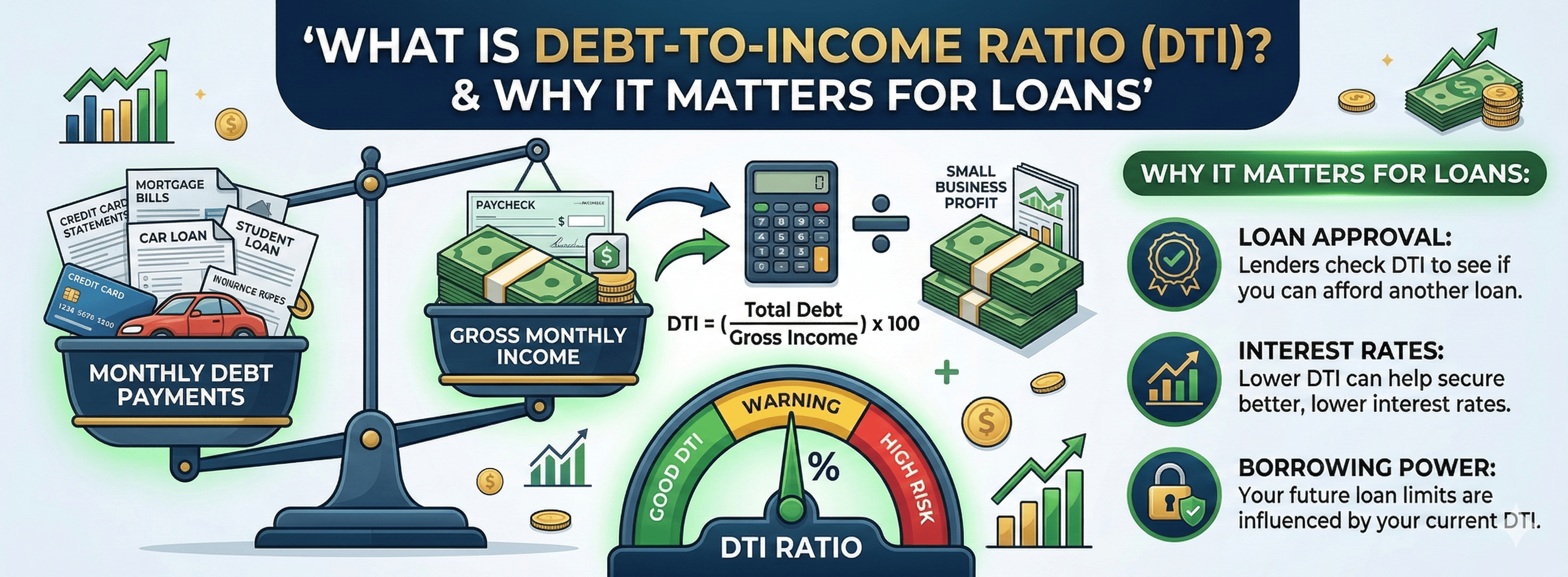

Your debt-to-income ratio shows how much of your monthly income is already committed to paying debts. Lenders use this ratio to determine whether you can comfortably repay a new loan.

A high DTI ratio may reduce your chances of loan approval, while a lower ratio indicates stronger repayment capacity.

In this guide, we will explain what DTI means, how it is calculated, and why it is important for loan approvals.

What is Debt-to-Income Ratio (DTI)?

The Debt-to-Income Ratio (DTI) is a financial metric that compares your total monthly debt payments with your monthly income.

It measures how much of your income is used to pay existing debts.

Lenders use this ratio to determine whether a borrower can afford additional loans without financial strain.

DTI is expressed as a percentage.

Debt-to-Income Ratio Formula

The formula used to calculate DTI is simple.

DTI = (Total Monthly Debt Payments ÷ Monthly Income) × 100

Where:

Total Monthly Debt Payments include:

• Personal loan EMIs

• Home loan EMIs

• Car loan EMIs

• Credit card minimum payments

Monthly income refers to your gross monthly income before deductions.

Example of Debt-to-Income Ratio Calculation

Let us consider a practical example.

Monthly income: ₹60,000

Existing debts:

Home loan EMI: ₹15,000

Car loan EMI: ₹5,000

Credit card payment: ₹2,000

Total monthly debt payments: ₹22,000

DTI calculation:

DTI = (22,000 ÷ 60,000) × 100

DTI = 36.6%

In this example, the borrower has a debt-to-income ratio of around 37%.

Ideal Debt-to-Income Ratio for Loan Approval

Most lenders prefer borrowers with a DTI ratio below 40%.

DTI Ratio — Loan Approval Impact

Below 30% — Excellent financial profile

30–40% — Good eligibility

40–50% — Moderate risk

Above 50% — High risk for lenders

A lower DTI ratio improves your chances of getting loan approval and may also help secure better interest rates.

Why Debt-to-Income Ratio is Important

DTI is a key indicator of financial health and repayment capacity.

Helps Lenders Evaluate Risk

A lower DTI suggests that the borrower has enough income to repay loans comfortably.

Determines Loan Eligibility

Banks often use DTI to calculate the maximum loan amount a borrower can afford.

Affects Interest Rates

Borrowers with lower DTI ratios may receive better loan terms and lower interest rates.

Prevents Overborrowing

DTI helps lenders ensure that borrowers do not take loans they cannot afford.

Types of Debt Considered in DTI

When calculating DTI, lenders usually include the following obligations.

• Home loan EMIs

• Personal loan EMIs

• Car loan payments

• Credit card dues

• Education loan EMIs

• Other recurring loan obligations

Regular household expenses such as rent, groceries, and utility bills are usually not included.

How DTI Affects Different Loans

Debt-to-income ratio is considered in almost every loan application.

Home Loans

Banks carefully evaluate DTI for home loans because they involve large loan amounts and long repayment periods.

Personal Loans

Since personal loans are unsecured, lenders use DTI to assess repayment capacity.

Car Loans

A high DTI ratio may reduce the loan amount approved for vehicle financing.

Credit Cards

DTI may influence credit card limits and approvals.

How to Reduce Your Debt-to-Income Ratio

If your DTI ratio is high, you can improve it using several strategies.

Pay Off Existing Debts

Clearing small loans or credit card balances reduces monthly debt obligations.

Increase Your Income

Higher income automatically reduces the DTI percentage.

Avoid Taking Multiple Loans

Applying for too many loans increases your debt burden.

Consolidate Debts

Combining multiple debts into a single loan can simplify repayment and reduce interest costs.

Limit Credit Card Usage

High credit card balances increase monthly debt obligations.

Relationship Between DTI and Credit Score

Although DTI and credit score are different metrics, both influence loan approval.

Credit score reflects your repayment history and credit behavior.

DTI reflects your current financial obligations compared to income.

Lenders typically evaluate both factors before approving a loan.

Frequently Asked Questions

What is a good debt-to-income ratio?

A DTI ratio below 40% is generally considered healthy for loan approval.

Can I get a loan with high DTI?

It may still be possible, but lenders may approve smaller loan amounts or charge higher interest rates.

Does DTI affect credit score?

DTI itself does not directly affect your credit score, but high debt levels can indirectly impact your credit profile.

How can I calculate my DTI ratio?

You can calculate it by dividing your total monthly debt payments by your monthly income.

Conclusion

The Debt-to-Income Ratio (DTI) is one of the most important financial metrics lenders use to evaluate loan applications.

It helps banks determine whether borrowers have enough income to handle additional debt responsibly.

Maintaining a low DTI ratio improves your chances of loan approval and helps secure better interest rates.

Before applying for any loan, it is always advisable to calculate your DTI ratio, manage existing debts carefully, and ensure your financial obligations remain within manageable limits.

By maintaining healthy financial habits, borrowers can improve their eligibility and make smarter borrowing decisions.