Debt Consolidation Loan – Combine Multiple Loans into One EMI (2026 Guide)

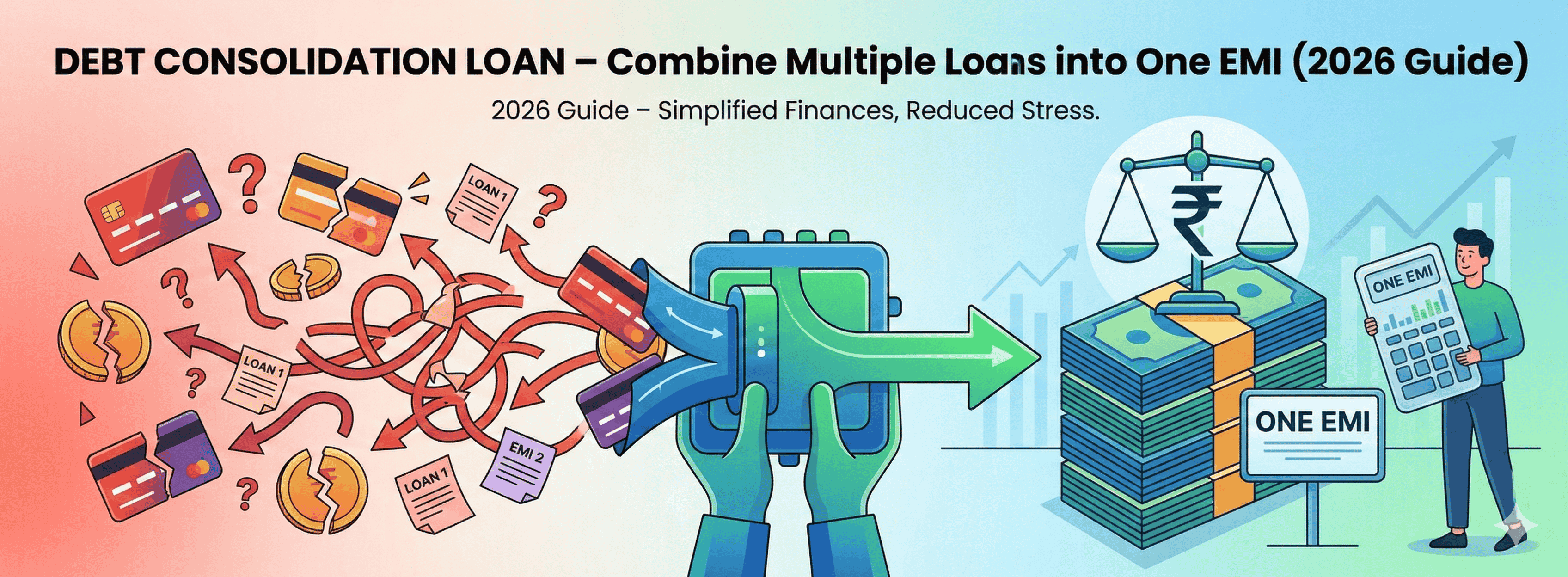

Managing multiple loans and credit card payments can become stressful and confusing. Many borrowers struggle to keep track of different EMIs, payment dates, and interest rates. This is where a Debt Consolidation Loan can be extremely helpful.

A debt consolidation loan allows borrowers to combine multiple debts into a single loan with one monthly EMI. Instead of paying several lenders separately, you only need to manage one loan repayment.

In this guide, we will explain how debt consolidation loans work, their benefits, eligibility requirements, and when you should consider using them.

What is a Debt Consolidation Loan?

A Debt Consolidation Loan is a financial solution that combines multiple outstanding debts into one single loan.

Borrowers often use personal loans to consolidate debts such as:

• Credit card balances

• Personal loans

• Payday loans

• Consumer loans

• Small unsecured loans

After consolidating these debts, borrowers only need to pay one EMI each month instead of multiple payments.

How Debt Consolidation Works

Debt consolidation works in a simple way.

Step 1: Borrower applies for a consolidation loan

Step 2: The loan amount is used to pay off existing debts

Step 3: All previous debts are cleared

Step 4: Borrower repays only the new consolidated loan

This simplifies debt management and can reduce financial stress.

Example of Debt Consolidation

Let us consider a practical example.

A borrower currently has the following debts:

Credit Card Debt — ₹1,50,000 — 36% interest

Personal Loan — ₹2,00,000 — 16% interest

Consumer Loan — ₹1,00,000 — 18% interest

Instead of paying three different EMIs, the borrower takes a debt consolidation loan of ₹4,50,000 at a lower interest rate.

Now the borrower pays one EMI with potentially lower interest and simpler repayment.

Benefits of Debt Consolidation Loans

Simplified Loan Management

Managing multiple EMIs can be confusing. Debt consolidation reduces everything to a single monthly payment.

Lower Interest Rates

Personal loan interest rates are often lower than credit card interest rates.

Better Financial Planning

With one EMI, borrowers can manage their monthly budget more efficiently.

Reduced Financial Stress

Instead of remembering several due dates, borrowers only need to track one payment.

Improved Credit Score

Timely repayment of a consolidation loan can improve credit scores over time.

Who Should Consider Debt Consolidation?

Debt consolidation may be useful for individuals who:

• Have multiple credit card debts

• Are paying high interest rates

• Have difficulty managing multiple EMIs

• Want a more organized repayment plan

However, it is important to ensure that the new loan has a lower interest rate than existing debts.

Eligibility for Debt Consolidation Loan

Eligibility for a consolidation loan is similar to personal loan requirements.

Typical criteria include:

Age between 21 and 60 years

Stable source of income

Minimum monthly salary of ₹20,000–₹25,000

Credit score above 700

Higher credit scores increase the chances of approval and lower interest rates.

Documents Required for Debt Consolidation Loan

To apply for a consolidation loan, borrowers typically need the following documents.

• PAN Card

• Aadhaar Card or address proof

• Salary slips or income proof

• Bank statements

• Details of existing debts

Some lenders may also request credit card statements or loan statements.

When Debt Consolidation May Not Be a Good Idea

While consolidation can be helpful, it may not always be the best option.

Avoid consolidation if:

• The new loan has a higher interest rate

• You plan to take new debts after consolidation

• You cannot maintain EMI discipline

Responsible financial behavior is important to ensure consolidation works effectively.

Tips for Successful Debt Consolidation

Choose Lower Interest Loan

Always ensure the new loan has a lower interest rate than existing debts.

Avoid Taking New Debt

After consolidating, avoid accumulating new credit card balances.

Create a Repayment Plan

Track EMI payments carefully to avoid missed payments.

Maintain Good Credit Score

Pay EMIs on time to improve your credit profile.

Debt Consolidation vs Balance Transfer

Borrowers often confuse debt consolidation with balance transfer.

Debt Consolidation

• Combines multiple debts into one loan

• Often done using personal loans

Balance Transfer

• Transfers one loan to another lender with lower interest

• Usually applies to home loans or credit cards

Both strategies aim to reduce interest costs but work differently.

Conclusion

A Debt Consolidation Loan can be an effective financial tool for borrowers struggling with multiple debts. By combining various loans into a single EMI, borrowers can simplify repayments and potentially reduce interest costs.

However, before choosing this option, it is important to compare interest rates, understand loan terms, and commit to responsible financial management.

When used correctly, debt consolidation can help borrowers regain control of their finances and work toward becoming debt-free.