How Credit Card Interest Works in India (2026 Complete Guide)

Credit cards are one of the most convenient financial tools available today. They allow users to make purchases without paying immediately and offer a grace period before payment is due.

However, many people are surprised by the high interest charges on credit cards when they fail to pay the full outstanding amount on time.

Understanding how credit card interest works is essential to avoid unnecessary financial costs and maintain healthy credit habits.

In this guide, we will explain how credit card interest is calculated in India, why it is often high, and how you can avoid paying excessive charges.

What is Credit Card Interest?

Credit card interest is the cost charged by the bank when you do not pay your full credit card bill by the due date.

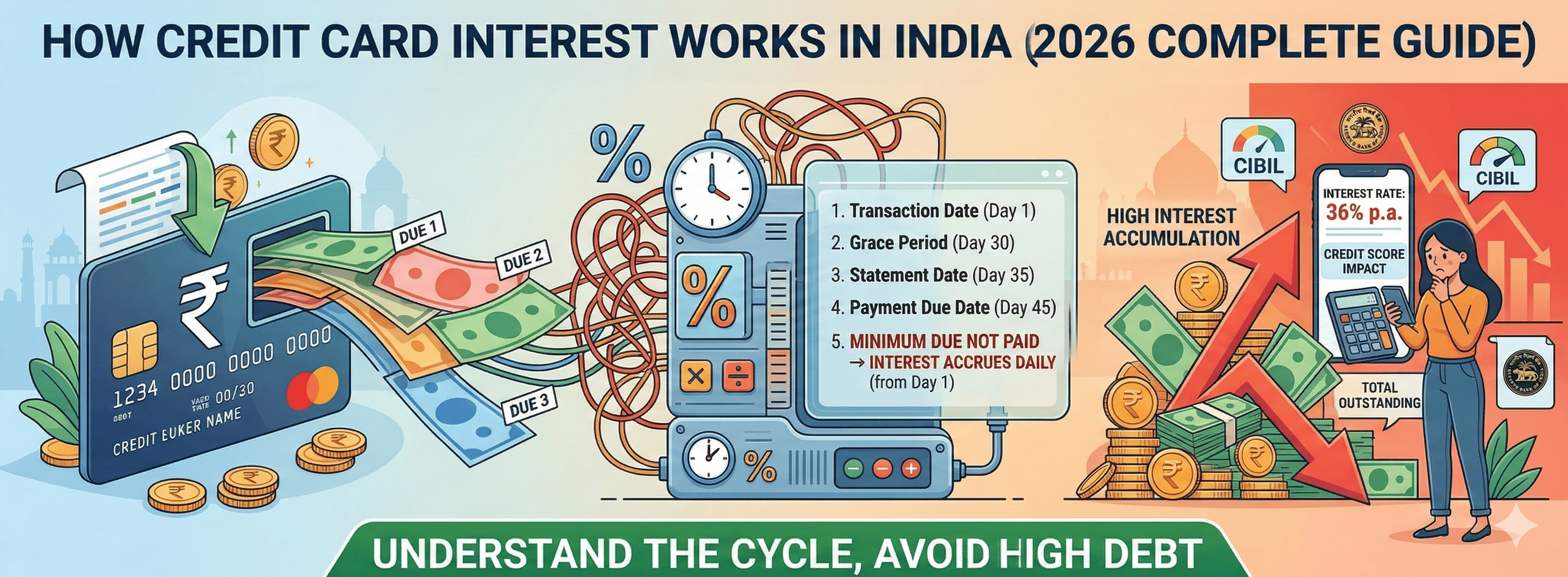

If you clear the entire outstanding amount within the billing cycle, most credit cards offer a grace period of 20–50 days, during which no interest is charged.

However, if you pay only the minimum amount due or miss the payment deadline, interest is charged on the remaining balance.

Typical Credit Card Interest Rates in India

Credit card interest rates in India are relatively high compared to other types of loans.

Typical ranges include:

Monthly Interest Rate: 2.5% – 3.5%

Annual Interest Rate (APR): 30% – 42%

This high interest rate is why credit card debt can grow quickly if not managed properly.

How Credit Card Interest is Calculated

Credit card interest is usually calculated on a daily outstanding balance.

Banks calculate interest using the following concept:

Daily interest = Outstanding balance × (Annual interest rate ÷ 365)

Interest is then accumulated daily until the outstanding balance is fully paid.

Example of Credit Card Interest Calculation

Let us consider a simple example.

Outstanding credit card balance: ₹50,000

Annual interest rate: 36%

Daily interest rate = 36% ÷ 365 ≈ 0.0986%

Daily interest = ₹50,000 × 0.0986% ≈ ₹49.3

If the balance remains unpaid for 30 days, the total interest charged may be around ₹1,479.

This shows how quickly interest can accumulate on unpaid credit card balances.

What Happens If You Pay Only Minimum Amount Due?

Credit card statements usually display a Minimum Amount Due (MAD).

This amount is typically around 5% of the total outstanding balance.

If you pay only the minimum amount:

• Your account remains active

• You avoid late payment penalties

• Interest continues to accumulate on the remaining balance

Over time, this can lead to very high interest costs.

Credit Card Billing Cycle Explained

The billing cycle is the period during which your credit card transactions are recorded.

A typical billing cycle lasts 30 days.

After the billing cycle ends:

• A statement is generated

• A payment due date is assigned (usually 15–20 days later)

If the full amount is paid before the due date, no interest is charged.

Grace Period on Credit Cards

Most credit cards offer an interest-free grace period.

This period includes:

Billing cycle (30 days) + Payment period (15–20 days)

Total interest-free period: up to 45–50 days

However, this benefit only applies if the full outstanding balance is paid.

When Interest Starts Applying

Interest begins to apply when:

• You pay only the minimum due

• You miss the payment deadline

• You carry forward an unpaid balance

• You withdraw cash using your credit card

Cash withdrawals typically start accumulating interest immediately without a grace period.

Additional Charges on Credit Cards

Apart from interest charges, credit cards may also include additional fees.

Some common charges include:

• Late payment fees

• Cash withdrawal fees

• Foreign transaction charges

• Over-limit penalties

These charges can increase the total cost of using a credit card.

How to Avoid Credit Card Interest

Credit cards can be extremely useful if managed properly.

Here are some tips to avoid interest charges.

Pay the Full Bill Amount

Always try to pay the entire outstanding amount before the due date.

Track Your Billing Cycle

Understanding your billing cycle helps you maximize the interest-free period.

Avoid Cash Withdrawals

Credit card cash withdrawals usually attract immediate interest and high fees.

Set Payment Reminders

Automatic reminders can help prevent missed payments.

Use Credit Cards Responsibly

Avoid spending more than you can repay comfortably.

Impact of Credit Card Interest on Credit Score

High credit card balances and missed payments can negatively affect your credit score.

Important factors that influence credit score include:

• Payment history

• Credit utilization ratio

• Length of credit history

• Number of credit inquiries

Maintaining low credit card balances and timely payments helps maintain a healthy credit score.

Frequently Asked Questions

What is the average credit card interest rate in India?

Most credit cards charge interest between 30% and 42% annually.

Is credit card interest charged daily?

Yes, most banks calculate interest based on the daily outstanding balance.

What happens if I miss a credit card payment?

You may be charged late payment fees and interest on the outstanding amount.

Can I avoid interest if I pay the full amount?

Yes, paying the full statement amount before the due date avoids interest charges.

Conclusion

Credit cards offer convenience and financial flexibility, but they must be used responsibly to avoid high interest charges.

Understanding how credit card interest works helps users make smarter financial decisions and avoid unnecessary debt.

By paying the full balance on time, tracking spending, and avoiding unnecessary charges, credit card users can enjoy the benefits of credit cards without falling into costly interest traps.

Responsible credit usage also improves credit scores and strengthens long-term financial health.